When the time comes to replace your roof, the last thing you want to worry about is whether you can afford it. Your roof protects everything under it: your family, your belongings, and your peace of mind. But when you start researching costs, it’s easy to get overwhelmed with numbers, terms, and financing jargon. If you’ve ever wished there was a simple, straightforward guide that breaks it all down for you, then you’ve come to the right place.

Unlike buying a new appliance, a roof isn’t just about material costs. The size of your home, the slope of your roof, the type of shingles, and labor all come into play. That’s why roof replacements can range from a few thousand dollars to tens of thousands. According to the U.S. Department of Housing and Urban Development (HUD), roofing is considered a major home system replacement, which makes financing an important tool for many families.

Think of roof financing like choosing how to buy a car: you can pay cash, take out a loan, or set up a payment plan. Each option comes with pros and cons, and understanding them can make the decision much less intimidating. Let’s break down the most common ones.

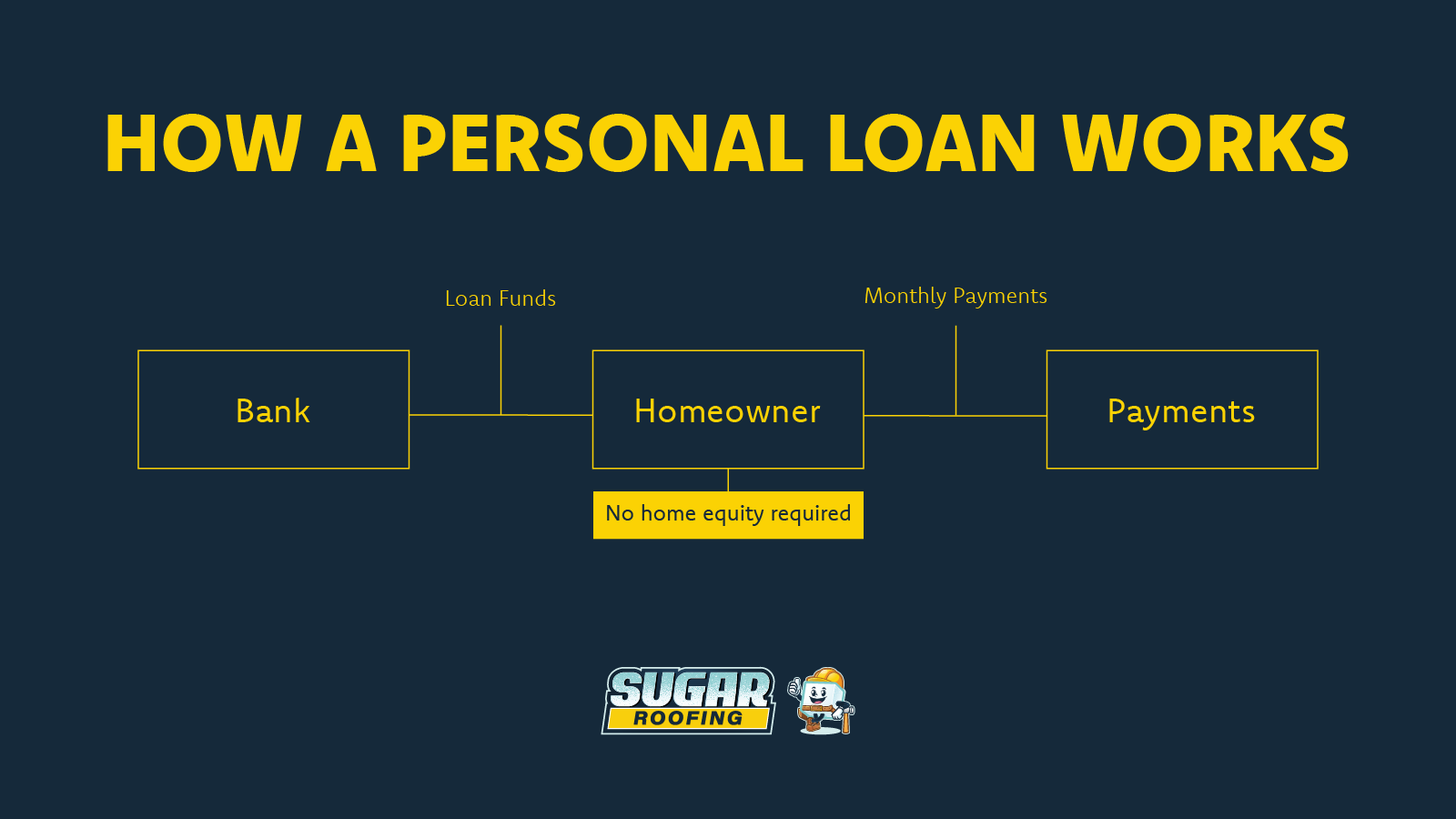

A personal loan is like borrowing a set amount of money from a bank or lender, then paying it back over a set period. Many homeowners like this option because it doesn’t require you to put your home up as collateral. Interest rates can vary based on your credit score. The Consumer Financial Protection Bureau (CFPB) has a simple guide on how personal loans work.

If you’ve built equity in your home, you can borrow against that equity. A home equity loan is a lump sum loan with a fixed rate, while a HELOC (Home Equity Line of Credit) works more like a credit card, where you borrow what you need up to a limit. According to the Federal Trade Commission (FTC), these loans often have lower interest rates, but your home is the collateral.

Some homeowners choose to put their new roof on a credit card, especially if they qualify for a 0% introductory APR offer. This can be helpful if you can pay it off quickly, but it can also become expensive if balances carry over. The CFPB warns that interest rates on credit cards are usually higher than on other loans.

Many roofing companies, including Sugar Roofing, offer in-house or partnered financing options. These are designed specifically for roof replacements and often come with flexible terms. Since approval can be faster and more straightforward, this option is worth asking about when you get your estimate.

For Sugar Roofing, we offer flexible plans starting at $99/month, with options for 0% interest up to 12 months. Our team will walk you through the approval process during your estimate or consultation. Get a free estimate here.

Sometimes, homeowners don’t have to shoulder the whole cost themselves. If your roof damage comes from storms, hail, or fire, your homeowners' insurance may cover part of the replacement. You can check coverage details in your policy or through USA.gov’s Homeowners Insurance Guide.

Additionally, the federal government offers certain financing and assistance programs:

Choosing the right financing is like choosing the right roof material — it depends on your home, your budget, and your long-term goals. If you want predictable payments, a personal loan or home equity loan may be best. If you want flexibility, a HELOC or credit card might work. And if you want something tailored to roofing, a company financing program could be the winner.

Beyond the type of loan, keep these things in mind:

Replacing your roof is one of the biggest investments you’ll make in your home, but the good news is, you don’t have to pay for it all at once. With financing options like personal loans, HELOCs, FHA Title I loans, and company programs, you can spread the cost out in a way that makes sense for you. The best way to know what’s right for your home and budget is to talk to a roofing professional who can walk you through both your roofing needs and financing options. To get started, contact Sugar Roofing today for a free roof replacement estimate.